DSCC

[email protected]

FOR IMMEDIATE RELEASE: 09/30/2024

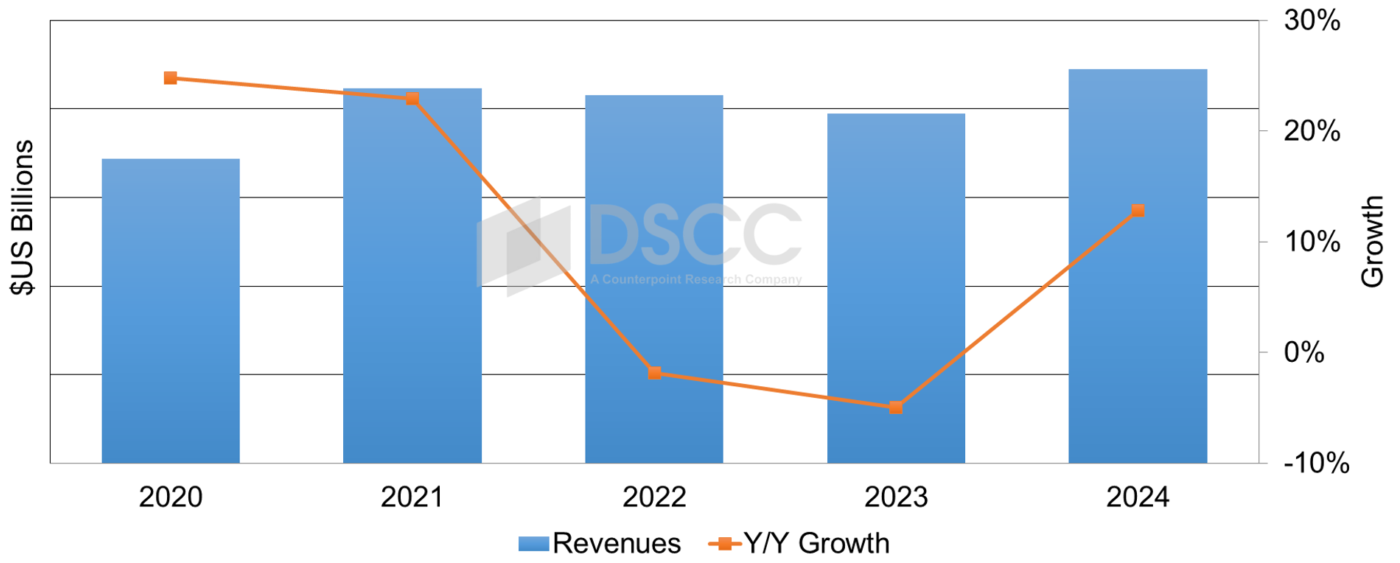

OLED Revenues Expected to Increase 13% in 2024 on Growth from Smartphones, TVs and IT Applications

La Jolla, CA -

- Q2’24 OLED revenues rose 36% Y/Y on 49% Y/Y unit growth.

- 2024 OLED revenues are expected to increase 13% Y/Y on 22% unit growth helped by a richer mix.

- 2024 OLED tablet revenues are expected to rise 584% Y/Y on 221% unit growth.

As revealed in DSCC’s latest release of the OLED Shipment Report, OLED panel revenues increased 36% Y/Y in Q2’24. The improvement to panel revenues is the result of the 49% Y/Y unit increase as a result of improved consumer and commercial demand offset by seasonality for some applications. In Q2’24, OLED monitors and tablets had triple-digit unit and revenue growth Y/Y. Several other applications had Y/Y increases. Please refer to the report for more details.

In Q2’24, by select OLED applications:

- OLED smartphone units increased 49% Y/Y and 24% Y/Y in revenues on 49% Y/Y increases for rigid OLED smartphones, 32% Y/Y unit increases for flexible OLED smartphones and 120% Y/Y unit increases for foldable OLED smartphones with double-digit panel ASP declines for flexible and foldable OLEDs;

- OLED TVs increased 30% Y/Y in units and 36% Y/Y in revenues;

- OLED monitors increased 157% Y/Y in units and 111% Y/Y in revenues. OLED tablets had 356% Y/Y unit growth >1000% Y/Y revenue growth as a result of the introduction of Apple’s 11.1” and 13” iPad Pro models.

By panel supplier for all applications, we expect SDC to lose revenue share as a result of gains from China Star, LGD, Tianma and Visionox.

AMOLED Panel Revenue and Y/Y Growth, 2020 – 2024

The latest OLED Shipment Report includes updates to market forecasts as well as updates for panel supplier and brand roadmaps.

About Counterpoint

Counterpoint Research is a global market research firm specializing in products across the technology ecosystem. We advise a diverse range of clients – from smartphone OEMs to chipmakers and channel players to Big Tech – through our offices located in the world's major innovation hubs, manufacturing clusters and commercial centers. Our analyst team, led by seasoned experts, engages with stakeholders across the enterprise – from the C-suite to professionals in strategy, analyst relations (AR), market intelligence (MI), business intelligence (BI), product and marketing – to deliver services spanning market data, industry thought leadership and consulting. Our core areas of coverage include AI, Automotive, Consumer Electronics, Displays, eSIM, IoT, Location Platforms, Macroeconomics, Manufacturing, Networks and Infrastructure, Semiconductors, Smartphones and Wearables. Visit our Insights page to explore our publicly available market data, insights and thought leadership, and to understand our focus, meet our analysts and start a conversation.