DSCC

[email protected]

FOR IMMEDIATE RELEASE: 11/25/2024

Double-Digit Y/Y Growth for Smartphones and TVs Fuel 32% Y/Y Growth for OLED Panel Shipments in Q3’24

La Jolla, CA -

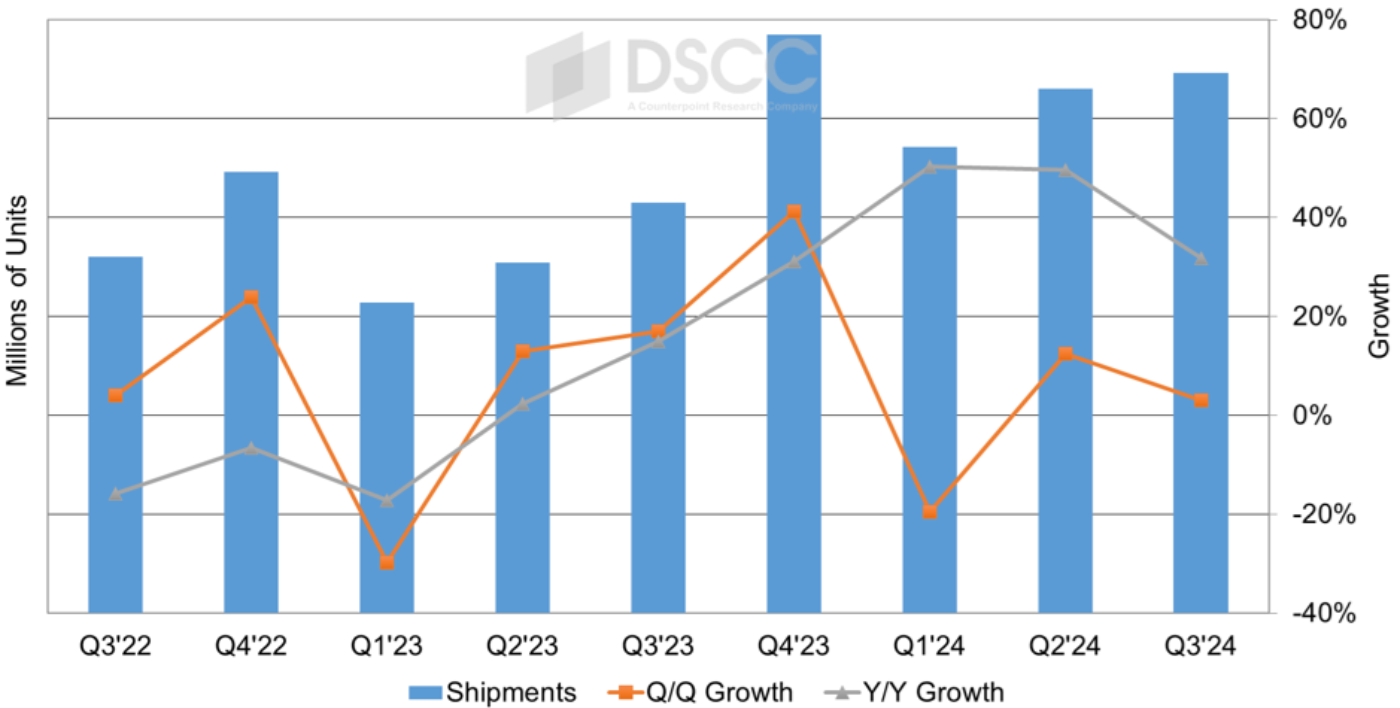

- In Q3’24, OLED panel shipments increased 32% Y/Y, led by growth from smartphones, TVs, monitors notebook PCs and tablets.

- In Q3’24, for OLED smartphones, several brands had double-digit Y/Y growth resulting in the category achieving 39% Y/Y growth.

- Samsung Display continues to lead with double-digit share for all OLED applications.

As revealed in DSCC’s latest release of the OLED Shipment Report – Flash Edition, OLED panel shipments increased 3% Q/Q and 32% Y/Y in Q3’24 after increasing 12% Q/Q and 50% Y/Y in Q2’24. In Q3’24, by select OLED applications, OLED tablet panel shipments decreased 20% Q/Q and increased 127% Y/Y, OLED smartphones increased 2% Q/Q and 39% Y/Y and OLED TVs increased 2% Q/Q and 48% Y/Y.

“The continued double-digit Y/Y growth for OLED panel shipments is welcomed news that strong demand continues for OLED applications. We expect 2024 to have double-digit Y/Y growth, fueled by increased demand in the commercial and consumer PC sector and AI innovations across several categories,” notes David Naranjo, Sr. Director.

OLED Panel Shipments and Y/Y Growth, Q3’22 – Q3’24

By OLED panel supplier, SDC continues to lead in OLED panel shipments with a 37% overall share, down from 40% in Q2’24, as a result of gains from LGD and Visionox. LGD’s share increased to a 13% share, up from 8% in Q2’24 as a result of 49% Q/Q and 204% Y/Y growth from OLED smartphones, fueled by Apple with a 65% Q/Q and 69% Y/Y increase.

The OLED Shipment Report – Flash Edition, includes historical panel shipments from 2016 through Q3’24 by application, by brand, by panel supplier, by OLED type and much more.

About Counterpoint

Counterpoint Research is a global market research firm specializing in products across the technology ecosystem. We advise a diverse range of clients – from smartphone OEMs to chipmakers and channel players to Big Tech – through our offices located in the world's major innovation hubs, manufacturing clusters and commercial centers. Our analyst team, led by seasoned experts, engages with stakeholders across the enterprise – from the C-suite to professionals in strategy, analyst relations (AR), market intelligence (MI), business intelligence (BI), product and marketing – to deliver services spanning market data, industry thought leadership and consulting. Our core areas of coverage include AI, Automotive, Consumer Electronics, Displays, eSIM, IoT, Location Platforms, Macroeconomics, Manufacturing, Networks and Infrastructure, Semiconductors, Smartphones and Wearables. Visit our Insights page to explore our publicly available market data, insights and thought leadership, and to understand our focus, meet our analysts and start a conversation.